Spotlight | Inflation and Interest Rates

This communication is provided FOR INTERNAL USE ONLY so please don’t share the link with anyone outside NorthRock.

Introduction

The phenomenon of inflation is a capricious and elusive force in markets. Inflation is the measurement of the change in aggregate prices for goods and services in the economy over a given period. The most common indices measuring inflation today are the Consumer Price Index (CPI) and the Personal Consumption Expenditures Index (PCE). Both indices attempt to measure the change in prices (1) that consumers pay for goods and services.

While consistent and moderate inflation is healthy for an economy, it can become a problem if it runs too hot or too cold. Like Goldilocks and her quest to find a “just right” temperature for her porridge, central banks globally are on a mission to target a level of inflation that is “just right” for their respective economies.

Background

The Quantity Theory of Money suggests that over the long-term, inflation is equal to the money supply (how much money is in the system) multiplied by the velocity of money (how often money is flowing through the system), assuming equal levels of GDP (2). If the amount of money in the system increases and the velocity of money is constant, the cost of the same amount of goods and services should increase over time. Much is unknown about inflation and even this basic statement regarding money supply is often debated amongst economists. We know that some combination of the below have historically sparked and/or caused elevated levels of inflation:

Supply – When supply is low, the same number of participants bid up the price. In this scenario, there is no change in demand with less aggregate goods and services available for all participants.

Demand – When demand is higher, participants may look to purchase more of a good or service even though the supply is constant, thereby bidding up the price.

Budget Deficits – Excess budget deficits are the result of a government consistently spending more than it takes in. A government that spends more than it collects leads to increasing moneys outstanding and increasing levels of debt. This has resulted in inflation over the long term.

Future Expectations – If participants expect goods and services to cost more in the future, there is an incentive to purchase more goods today at a cheaper price. Deferring consumption can be costly given the expected future inflation. This creates an inflation spiral, which is explained in more detail below.

This last point highlights why a small amount of expected inflation is healthy for the economy: it incentivizes participants to spend and invest today as the price of goods and services are expected to increase in the future. If expected inflation were near zero, participants may be incentivized to save and invest for the future rather than spend today. The result could cause economic activity today to fall below trend and result in an economic slowdown or worse, deflation (3).

The Mechanics of Inflation and Interest Rates

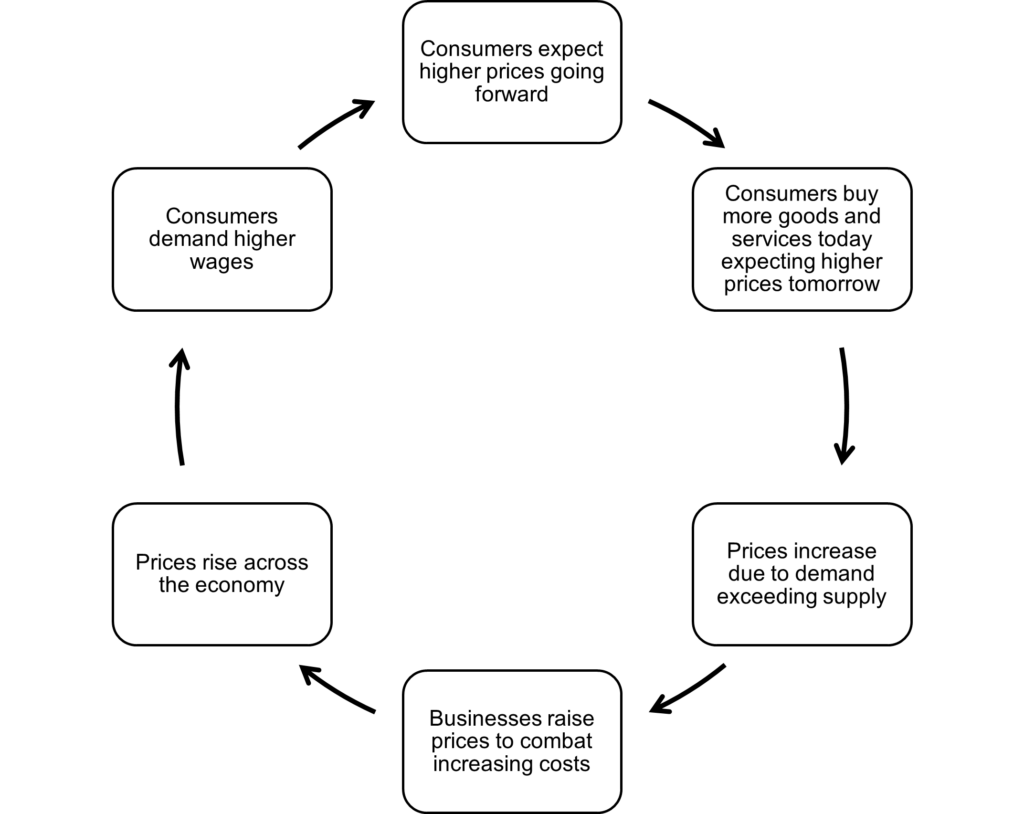

When inflation increases beyond a reasonable level, say 3%, it can be disruptive to economies and individuals. Given 3% inflation, prices for goods and services double around every 23 years. At 5% they double every 14 years, and at 7% they double every 10 years. The inflation cycle graphic below highlights the circular inflation spiral that can become entrenched when inflation increases.

The above is known as the “inflation spiral.” First, prices for goods and services increase, either slowly or due to a shock. Businesses respond by increasing prices to offset increased costs, which further increases the prices of goods and services throughout the economy. Participants begin to feel the burden of their budget costing more, and therefore demand higher wages. As wages increase, businesses continue to increase prices to offset increased costs (wages). This circular effect continues throughout the economy until something breaks, typically by declining demand in a recession.

The Federal Reserve (the “Fed”) is often the organization responsible for breaking an inflation spiral. The Fed, or the Central Bank of the United States, has a dual mandate to maintain price stability (targeting 2.0% long-term inflation) and full employment (a subjective measure of the highest level of sustainable employment which does not lead to excess inflation). The Fed aims to achieve these objectives via monetary policy, most notably by increasing or decreasing the cost to borrow on the Fed Funds Rate. This is the rate at which banks can borrow and lend and represents the floor for short-term rates. The Fed is the only group that can effectively increase or decrease the amount and cost of money in the system, and they act independently of the other branches of government.

- When the economy is entering a recession, the Fed can reduce interest rates to incentivize consumers and businesses to spend and borrow more, helping to increase demand and push the economy out of a recession.

- “Dovish”; monetary easing

- When the economy is overheating and/or experiencing high inflation, the Fed can increase interest rates to dissuade consumers and businesses to spend and borrow, thus slowing economic activity.

- “Hawkish”; monetary tightening

These tools are blunt by nature; the tools are slow to implement and often result in “overshooting” in both directions. Historically, it has been much easier for the Fed to quickly slow economic activity and more difficult to revive economic activity. The Fed aims to act as an independent organization that works counter-cyclically to economic activity by stimulating the economy during downturns and slowing the economy when it is overheating. The Fed has always been controversial because of the difficulties in achieving both mandates simultaneously, the politicization of the government budget, the intertwined political nature of fiscal policy, and natural pressures from the three branches of government.

As noted, sometimes both stable prices and full employment cannot be maintained simultaneously. This will result when the Fed is forced to engage in monetary tightening (increasing interest rates) because of an overheating economy or excess inflation. In this situation, the Fed has been clear that it will choose to first achieve stable prices at the cost of not achieving full employment. The rationale is that the Fed believes stable prices are the bedrock of the economy and are essential for a functioning system. In other words, the Fed does not believe that full employment can be achieved in the long-term if the economy does not first have stable prices (via controlled inflation).

A Brief History of Inflation

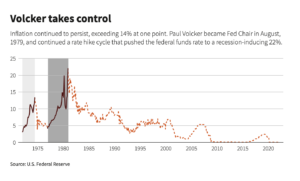

Inflation has existed for as long as money has been used to exchange goods and services. During the great Roman Empire, the Drachma saw 15,000% inflation from 200 AD to 300 AD (4). During the German Weimar republic, the monthly inflation rate of the papiermark was approximately 29,000% in October of 1923 (5). The US experienced inflation throughout the ‘70s and ‘80s that forced the Fed to raise rates multiple times in the ‘70s. Throughout this period, the Fed eased rates as the economy entered recessions without waiting for core inflation to remain below 3.0% for a material amount of time. Because the inflation was never truly dispelled, the expectations for inflation remained elevated and inflation never dipped below 6.0% throughout the late ‘70s until the early ‘80s. During this period, Fed President Paul Volcker increased interest rates from less than 5.0% in the late ‘70s to greater than 20% by ‘82. Volcker was criticized at the time for driving the economy into a recession but praised decades later for finally dispelling the near 20-year bout of inflation.

(6)

(6)

The Current Environment

Since the great financial crisis, there have been multiple loose fiscal and monetary policies that may have contributed to inflation:

- The Fed kept the Fed Funds rate at historic lows after the Great Financial Crisis through the late 2010s. The Fed Funds rate was briefly increased to 2.5% between 2016 and 2019 but was reduced back to zero during the Covid pandemic (7).

- The Fed engaged in open market bond purchases (dubbed “quantitative easing”) for the first time in 2008. This involves the Fed purchasing short-term government bonds and mortgage-backed securities to support liquidity. This effectively increases the supply of money and reduces yields. 2020 purchases in aggregate brought the Fed balance sheet assets above $7 trillion, peaking at over $8.9 billion in April 2022.

- The US government has increased the budget deficit, both as a percentage of GDP and in absolute dollar terms, to historical highs. Key fiscal policy decisions include the forgivable PPP loan to businesses, multiple rounds of stimulus checks sent to consumers during the Covid lockdowns, and the more recent student loan forgiveness. These policies effectively increase aggregate liquidity and the supply of money in the system.

As of October 2022, inflation has spiked to the highest levels since the ‘80s (8). The Fed is currently focused on increasing rates and stopped purchases of bonds (while letting current holdings mature). Both of these actions effectively reduce the amount of money in the system and increase the cost to borrow.

Impact on Asset Classes

Inflation impacts assets differently based on the mathematics of valuation, the flow through to the real economy, and the expected duration of the inflation.

Stocks

Equities are adversely impacted by inflation both via earnings compression and increased opportunity cost. Businesses have increased costs as prices rise, which reduce earnings all else equal. If earnings go down and the multiple (P/E) that investors pay on the earnings remains constant, the equity will be worth less. Some businesses are better at weathering costs, adjusting debt and contracts, pushing cost increases to suppliers (controlling margins), and pushing cost increases to customers (increasing revenue).

Mathematically, the value of equities is equal to the estimated future stream of free cash flows that the business produces, discounted to the present. They are discounted at a rate that is equal to a risk-free rate (usually a longer-term US treasury) and an added equity risk premium. Equities are discounted at a higher rate as inflation increases because US treasury yields increase. This is easy to remember as an opportunity cost; as inflation increases and the yield on US treasuries increases, equities become less appealing relative to lower-risk treasuries that offer higher yields. The math is more impactful as inflation is expected to last for longer.

Bonds

As yields on US treasuries increase, fixed income yields increase across the board because the risk-free opportunity cost is higher. An incremental buyer of any fixed income instrument would require at least the risk-free yield plus a spread for the additional risk on the fixed income instrument. As yields increase, the price of fixed income instruments declines. Additionally, inflation can often bring about times of economic stress wherein the spreads (yield minus the risk-free rate) on fixed income instruments also increases. This is because of an increase in the perceived probability of default on the underlying business or asset.

Alternative Assets

Alternative assets can mean many things. To keep this topical and short, we will discuss real assets, which includes real estate and natural resources. Mortgage rates are typically based on the 10-year treasury plus a spread for the underwriters (banks or loan underwriting businesses). Mortgage rates increase for the same reasons as fixed income: the risk-free rate increases and/or the spread increases. As mortgage rates increase, the gross real estate value that a mortgage can purchase with the same amount of money declines. Rents generally increase with inflation, so the value of rental properties is known to be relatively inflation resistant. Natural resources generally hold value to inflation over time and are considered one of the purest inflation hedges in a portfolio. The cost to produce the commodities increases in an inflationary environment and is passed along to the buyer via higher prices. Commodities are notably volatile based on supply, demand, and input costs. Input costs include oil and gas prices as well as freight costs.

Conclusion

Inflation is difficult to predict and based on a dynamic and ever-changing relationship between current prices and future expectations. The Fed is constantly trying to find a balance by interpreting how its dual mandate of maintaining price stability and full employment is impacting markets. Inflation, interest rates, and the Fed are interwoven in headlines today, encompassing much of the market news. We will continue to monitor interest rate and inflation developments given their uncertainty as well as their impact on asset classes and markets.

Sources

1 Bls.gov paper article highlighting differences between CPI and PCE: https://www.bls.gov/opub/btn/archive/differences-between-the-consumer-price-index-and-the-personal-consumption-expenditures-price-index.pdf

2 https://www.investopedia.com/insights/what-is-the-quantity-theory-of-money/

3 Deflation is the decline in prices for goods and services. A decline in prices could result in declining economic activity as participants defer purchases based on the belief that goods and services will be cheaper in the future.

4 https://dailyhistory.org/What_Role_Did_Inflation_Play_in_the_Collapse_of_the_Roman_Empire

5 https://www.cnbc.com/2011/02/14/The-Worst-Hyperinflation-Situations-of-All-Time.html

6 https://graphics.reuters.com/USA-FED/HIKES/mopandgebva/

7 https://fred.stlouisfed.org/series/MEDCPIM158SFRBCLE

8 Based on year-over-year rate of change.